Insurers argue their practices are appropriate, and that they are investing more into working through claims.

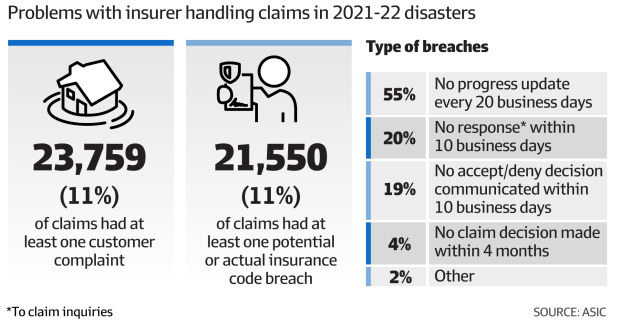

But the Australian Securities and Investments Commission warns problems remain overall with resourcing and oversight.

“We’re disappointed not to have seen further improvements from the insurers,” ASIC commissioner Alan Kirkland tells the Financial Review.

ASIC had last year detailed problems with insurers’ response to 2022 disasters, such as delays replacing a bloodied carpet for a customer talking about hurting themselves.

This year, ASIC warned insurers: lift your performance. Kirkland confirms also asking individual insurers how many claims remained unresolved and why they were unresolved.

“From that we’ll be forming a view around whether there are issues within particular insurers that require further action,” he says.

ASIC commissioner Alan Kirkland. Alex Ellinghausen

It’s ASIC’s latest blowtorch in the past few years about insurer transgressions. IAG, for instance, was sued about discount stuff-ups that detonated a record $40 million court fine. And that’s a fraction of expenses: IAG notched gross costs of more than $500 million fixing those discount debacles.

That raises questions of whether costly systemic issues could burst from claims handling. Kirkland says it is too early to say if large-scale remediation programs are required.

“If it’s clear that there are significant numbers of consumers who are out of pocket, then we’ll consider trying to have that situation righted,” he says.

Insurer reforms

Andrew lives in Logan, about 30 minutes’ drive south-east of Brisbane, and muddy stormwater inundated his home in 2022. Suncorp’s repair contractors left Andrew frustrated.

The dispute went to the Australian Financial Complaints Authority, which listed problematic repairs: the laundry sink, hallway plastering, off-kilter tiling on steps.

“Dealing with the insurer I was often facing very young people with no real-world experience simply reading a script … [they] simply rejected flatly any issues,” Andrew says.

On top of $21,611 already settled, AFCA recommended Suncorp pay $11,200. That included $2500 in non-financial compensation, partly because AFCA was “not satisfied” Suncorp had “acted appropriately and in a timely manner”.

Suncorp says it has dealt with more than 700,000 disaster claims in five years, does a good job in “the vast majority of cases”, and claims managers work with experts.

But a Suncorp spokeswoman acknowledges “we don’t always get it right”. The insurer was investing in people, culture and systems, she says. Suncorp also speaks to customer advocates, its supply chain and regulators to “gain invaluable feedback”.

Auto & General, whose brands include Budget Direct, argues it learned “valuable lessons” after 2022’s disasters and made “significant” resourcing and process changes.

IAG, whose brands include NRMA, lists adding an extra 150 employees to its 3800-strong claims team since March 2023, which can be bolstered with outsourced staff.

These are additional costs coming as disputes explode – insurance complaints to AFCA jumped 50 per cent last year to 27,924.

Some disputes are tinged with suspicion about tactics, including about cash payouts, where customers handle the responsibility of repairing damage.

Claims Hero, which earns money by acting for clients in disputes, has documentation indicating insurers can make cash-settlement offers with individual item costings blacked out.

“It makes it difficult for the consumer to assess whether the quote is sufficient,” Claims Hero managing director Luke Dugdell says. “It’s akin to a cashier only telling you the total cost of your groceries without itemising the prices.”

And incorrectly, in one email, a representative of Suncorp brand GIO initially wrote it does “not have legal rights to send out unredacted information”.

Claims Hero staff, which includes former Suncorp employees, have pushed back and successfully obtained the cost of line items.

Dugdell says one insurer, whom he declines to name, eventually released an unredacted quote that indicated some costings were provisional estimates – such as suspiciously $1000 round fee for supplying built-in wardrobes.

Another light installation only was priced as $91.50 for a new light, without listing associated costs of switches or labour, he says.

“The information supports the likelihood of variations,” he says. “If a customer were to have been cash-settled on the redacted [documentation], they would have received insufficient funds.”

In another case Dugdell cites, an insurance builder’s final works list left out items, such as two doors, which were only added later as a variation.

Insurer handling of claims in the 2022 floods was criticised. Mark Ludlow

Some insurers also seek quotes for “cash purposes only”. Dugdell argues this implies the builder was providing quotes “knowing the repairs will never be conducted by them”, and this could contribute to carelessness.

Suncorp’s own documentation in one such claim, however, maintained the quote could theoretically be carried out by its repairers, but the customer wanted cash.

Insurers can also offer cash quotes if they can’t complete repairs – perhaps a non-compliant pergola has damaged roof sheeting, for instance.

IAG, separately, says its final repair quotes can also be carried out by its builders, and customers can seek further settlement if their builders identify additional insurance-related damage during repairs.

Sources close to insurers maintained specific-item costs might be redacted to protect commercial secrets, but their builder quotes must be realistic. Buffers can be added to cash offers too.

Root causes of blunders?

An upstairs bathroom had leaked. It was 2020, IAG agreed to cover repairs and the home was dried out for 11 days. But two years later, the homeowner complained after finding mould under a stairwell.

IAG, while disputing the mould’s cause, agreed the original repairs were substandard. It obtained two rectification quotes: $6342.09 and $8817. (AFCA’s decision starkly notes the insurer acknowledged these quotes needed amendments as “the builders are not willing to do the quoted work for the quoted prices”.)

The customer’s quote was much bigger: $93,555, not including mould expenses. Ultimately, AFCA found IAG should pay $72,930 in rectification costs on two-year old repairs.

ASIC’s study last year found claims-handling problems were caused by issues including a lack of insurer oversight of contractors, poor communication and under-resourcing.

Claims Hero’s Dugdell, himself a former Suncorp assurance manager, alleges one factor potentially influencing poor outcomes is that repair contractors on insurer panels are in a highly competitive market, and insurers tend to choose providers offering the lowest quote.

“This behaviour, in turn, encourages other providers to adopt the same approach,” he says.

Insurers could not answer how often they chose the lowest quotes. But IAG maintained key factors in selecting repairers was their “quality, safe repairs and a high level of customer service”.

Other issues Dugdell alleges could contribute to poor outcomes are varying skill levels of some insurance practitioners, and that “some insurers impose time limits for processing tasks”.

On employment website Glassdoor, several people alleged they had worked in claims for Suncorp and were overwhelmed or monitored, even in phone-call durations.

“Management need to realise we deal with people who have had major loss. Staying on the phone longer with them should not be a black mark against our ability,” one wrote.

A source close to Suncorp maintains call metrics can be monitored to handle workforce demand for call centres, where customers might initially lodge claims.

But claims managers – actually working with customers after lodgment – are not subject to performance metrics or limits on individual calls, and encouraged to take time to help customers, the source says.

IAG says average call handling time is used to help forecast how many employees are needed.

Brisbane electrician Malcolm, still in dispute after two years, has used Claims Hero, and vast differences emerge in what he and the insurer think is needed to fix his home.

He questions paying “an awful lot” for insurance. “When you need them,” he says, “they don’t want to … cooperate.”