{kind=link}

Image source: Getty Images

One of my early investments in an ASX 200 stock is now up 618%, increasing sevenfold. It’s been a five-year journey that has provided a wealth of teachings along the way.

I’m a huge advocate of learning through doing. Nothing comes closer to the velocity and quality of education than what is gained by a baptism of fire. Hence, diving head-first into investing is, in my opinion, the best way to learn the art.

Reading is the second-best way. You can save (or make) a lot of money by applying the lessons learned by others. While I won’t claim to be any Warren Buffett, a few educational treasures from my experience might help the next person land a multi-bagger stock pick of their own.

Teachings from an ASX 200 healthcare stock

Pro Medicus Limited (ASX: PME) has become one of Australia’s greatest home-grown corporate success stories. The medical imaging software company was listed on the ASX in 2000 for $1.15 per share. Today, shares are worth north of $127.

I bought roughly $1,000 worth of this ASX 200 stock at a price of $17.75 in 2019.

Here’s what holding those 58 shares in Pro Medicus for a 600%+ gain has taught me.

Selling on valuation is a weak reason

There are many reasons to part ways with an investment — being ‘expensive’ is arguably the worst. Now, there’s a caveat here. Actions that erode the quality of the business can turn it into an overpriced asset. However, a large price tag in isolation shouldn’t make a company too expensive by default.

Warren Buffett, the world’s eighth richest person, once said, “Price is what you pay. Value is what you get.” Put differently, it matters what you’re getting for your money, not how much it is.

As shown above, Amazon.com Inc (NASDAQ: AMZN) shares traded on a price-to-earnings (P/E) ratio of about 300 times in late 2017. Yet, if an investor had sold on the premise of it being overvalued, they would have forgone the 217% rally since.

Quality matters more than price. Selling Pro Medicus shares based on its high P/E multiple — above 200 at times — never crossed my mind because the quality remained intact.

Don’t underestimate scalability

I didn’t fully appreciate the value of a scalable business until investing in this ASX 200 stock. Pro Medicus is a perfect example of how valuable a scalable product can be to a company and its shareholders.

The beauty of software, such as Pro Medicus’ Visage Imaging solution, is its incremental cost, which is oftentimes negligible. Furthermore, there’s no physical limitation to supplying increasing demand. If 50 new healthcare organisations wanted the software tomorrow, it would be nowhere near as difficult as supplying 50 companies with a fleet of Ford Rangers.

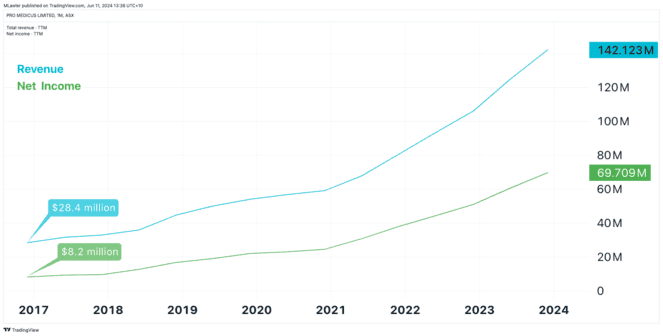

This is at the core of what makes scalable companies so appealing. Scalable companies can grow from a small business into a big-timer in a short window of time. For example, Pro Medicus’ revenue and net income have increased fivefold and nearly ninefold in less than a decade, as shown below.

You don’t need lottery tickets to win big

I know many aspiring investors who believe ‘taking a punt’ on a no-name company is the only way to achieve large gains in the stock market. Admittedly, I was one of them in my early days.

Such thinking might lead one to believe that Pro Medicus was an unheard-of, probably unprofitable, company when I first invested in it. Yet, that couldn’t be any further from the truth.

By March 2019, the ASX 200 stock generated $17.5 million in net profit after tax (NPAT) for the trailing 12 months at a 37.4% margin. It also had $32.3 million in cash (no debt) on its balance sheet. This is hardly reminiscent of a speculative mining explorer or drug developer.

The lesson here is you don’t need to dumpster dive for tomorrow’s great companies. You can buy the great companies of today and save yourself the added risk of an unproven business.