{kind=link}

Analysis by investment and advisory group Jarden Australia shows that purchasing an Australian home has increasingly become a multigenerational affair.

Jarden estimates that around 15% of borrowers are receiving an average of $92,000 from parents.

“If we assume the majority are first-home buyers, it would imply about 75% of first-home buyers were receiving some form of family assistance”, Jarden Australia chief economist Carlos Cacho said.

To add further insult to injury, 32% of first home buyers used various government loan schemes to get into the market in the 2022-23 financial year, according to data from the federal government agency Housing Australia (formerly the National Housing Finance and Investment Corporation).

Advertisement

Australia’s homeownership rate has trended down for decades, as illustrated below:

Source: Shane Oliver (AMP)

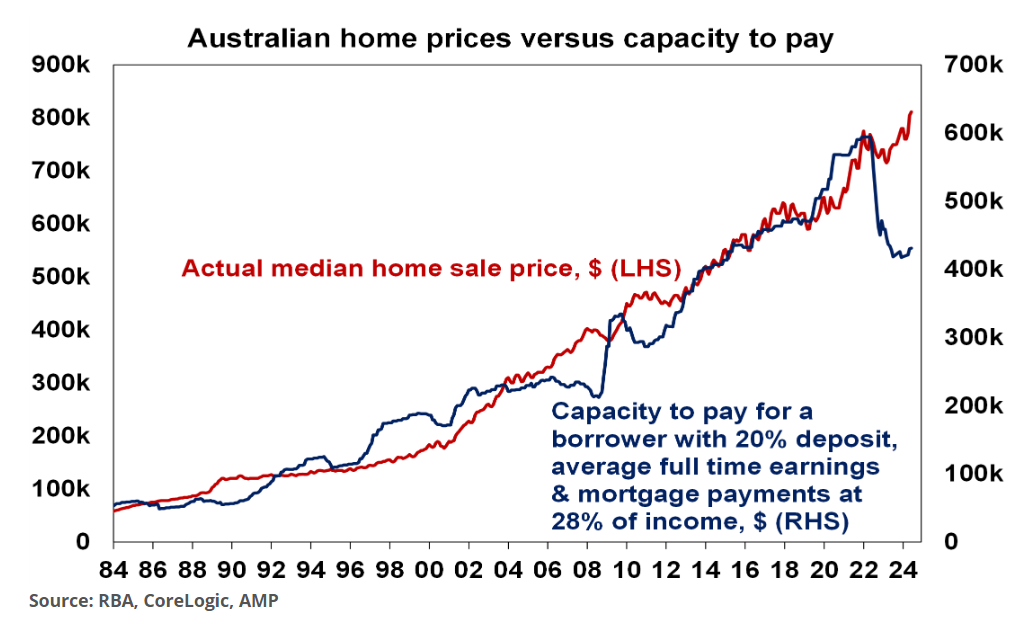

The gap between median dwelling values and capacity to pay has also widened since the Reserve Bank commenced its monetary tightening cycle:

Advertisement

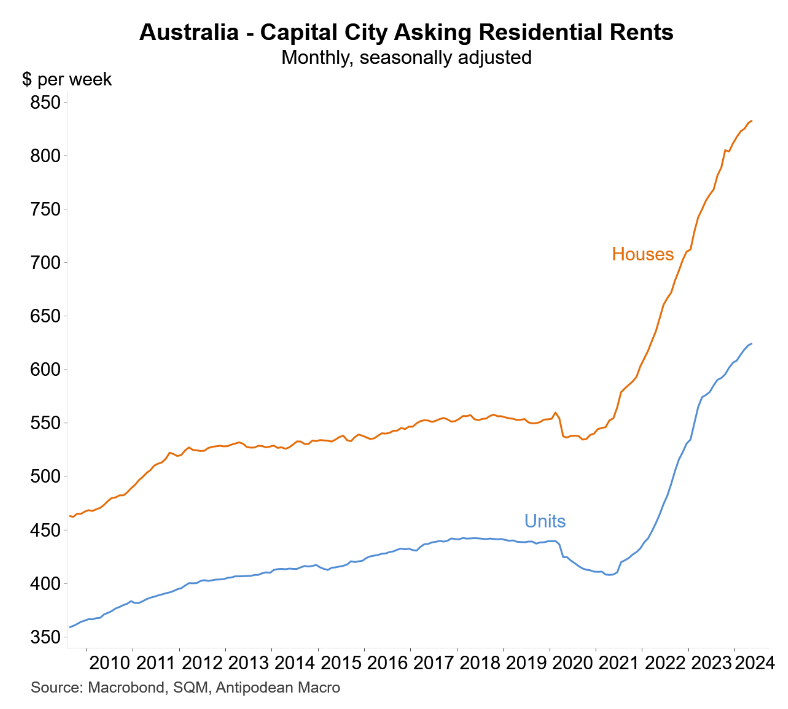

To make matters worse, the hyperinflation of rents has made it more difficult for would-be first home buyers to save a deposit:

Advertisement

The wicked combination of higher mortgage rates, record home prices, and soaring rents has meant that it has now become impossible for most first-time home buyers to purchase a home without family assistance.

The end result is that purchasing a home in Australia has become a multigenerational affair, with the ‘Bank of Mum & Dad’ and the ‘Bank of Grandma and Grandpa’ pooling together to push home prices higher.

Add the increase in foreign buyers and record immigration into the mix and you have a perfect storm for Australian housing affordability.

Advertisement

Economist Warren Hogan was right when he said that “FOMO on steroids” is feeding house prices.

“People have the view that the shortage is going to last for a long time and that will mean prices will just continue to rise”, Hogan told The AFR earlier in the month.

“Australia has never had a severe shortage like this in recent history, so this is a major market failure”.

Advertisement

“The reality is that there is price tension in the housing market because rents are going up, because of the shortage of rental property, which is underpinning demand from first-home buyers and investors”.

“It’s not just the bank of mum and dad, it’s also the bank of grandparents, or the bank of aunties and uncles. This is playing a much bigger role than it ever has before”, Hogan said.

Normally, 4.25% of rate rises from the Reserve Bank would have sent house prices plummeting.

The massive disparity between home prices and serviceability, however, serves as evidence that this is not a “normal” market.