{kind=link}

Image source: Getty Images

Fortescue Ltd (ASX: FMG) shares have had a gloomy past month. The iron ore miner’s 2024 decline has deepened by a painful 19.67% over the last 30 days. The recent slump means the company’s share price is now almost 28% lower than at the end of 2023.

The Fortescue share price is currently fetching $21.295, up 0.16% on yesterday’s closing value. Yet, today’s positivity is not contained solely to the Andrew Forrest-led miner. In fact, BHP Group Ltd (ASX: BHP) is basking in an even stronger showing, up 1.23% at the time of writing.

Back to Fortescue. Does the market’s current disinterest in the company present an opportunity to buy? After all, Warren Buffett — a billionaire investor — has said, “Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can’t buy what is popular and do well.”

Fortescue shares certainly don’t appear too popular at the moment, but could it be warranted?

Truckload of negativity

Investors have refrained from ‘buying the dip’ on Fortescue shares as they hurtle towards the 52-week low. The lack of price support coincides with several factors keeping the buyers at bay recently.

Firstly, the iron ore price is treading water. For nearly three years, prices have jumped momentarily, only to be magnetised back to around US$110 per tonne. Still, Fortescue can keep printing money at its US$18.93 per wet metric tonne C1 cost.

The problem is analysts expect iron ore to drop to US$95 a tonne, a forecast shared by Citi. The broker notes that the outlook for new construction in China is on loose footing, posing the case for weak iron ore demand.

Additionally, a major shareholder opted out of Fortescue shares last week. Capital Group Companies sold approximately $1.1 billion worth of the miner without providing any justification — the enormous sale adding to the market’s apprehension.

Lastly, the iron giant is still struggling to retain its executives. Julie Shuttleworth — who led the company’s efforts in Gabon, Africa — joined the executive exodus a couple of weeks ago.

The flip side to Fortescue shares

Every story has two sides, and it’s worth reviewing some of Fortescue’s positive attributes.

Fundamentally, Fortescue is in solid shape.

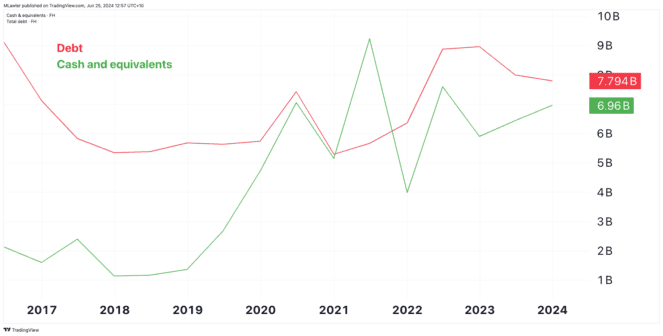

As shown above, the miner’s net debt has narrowed significantly compared to before 2020. This means Fortescue is financially healthier, better positioning the company to handle a downturn or fund growth initiatives.

Furthermore, its 12-month trailing free cash flow yield equates to 12.6%. For context, a free cash flow yield of around 5% is often considered attractive.

Likewise, the trailing dividend yield is a generous 9.6%, more than 6% greater than that offered by the S&P/ASX 200 Index (ASX: XJO). However, analysts expect this number to fall in line with reduced earnings in the coming years.

Foolish takeaway

Companies whose earnings are closely tied to the supply and demand of a commodity are difficult to value. You can’t simply extrapolate growth like you might with a candy bar or beverage maker. That’s not to say money can’t be made by investing in such businesses.

Fortescue has a competitive advantage in being one of the lowest-cost iron ore producers in the world. If the price of iron ore continues to fall, Fortescue should be able to keep making profits where others cannot.

Nevertheless, I’ll personally take my chances elsewhere than Fortescue shares.