Pending a potential appeal, Merchant is pursuing EY Australia and Burgess in court, alleging breach of contract and negligence in providing the advice. The case, which was launched in 2020, was delayed until the outcome of Merchant’s challenge to the Australian Taxation Office. EY and Burgess are defending the case.

EY said Justice Thawley’s judgment “only reflects a portion of the advice” given by the firm and could be subject to appeal. The firm said it was too early to characterise the judge’s findings on EY’s advice as conclusive.

But the emails make plain that from the very beginning, paying as little tax as possible from the sale of Plantic was Merchant and EY’s aim.

Burgess, who left EY in 2022, and McGrath spoke on July 9, 2014, and the EY partner advised that selling Plantic shares, rather than its assets, would be the best way to structure a deal. However, he said it would be necessary to deal with the $55 million in loans Plantic had from Merchant’s companies.

“If we were to sell Plantic what would the tax implications be for me?” Merchant emailed McGrath on July 21, 2014.

McGrath replied that: “EY have modelled it.”

“The way to go would be a share purchase by Sealed Air [a prospective buyer] of Plantic shares and not an asset purchase.”

McGrath outlined how EY believed Merchant should follow that plan and sell some of the high-cost Billabong shares he had from tipping into various capital raisings – as much as $7 a share when they were sitting around $2.60 on July 21, 2014 – from one company into his superannuation fund.

By doing this, Merchant would “get a good ‘loss’ on paper so they reckon there will be zero tax payable on a lump sum payment, which is very good”.

Merchant replied to McGrath that he was annoyed at EY for not alerting him to the need to pay taxes from his time in the United States.

“But I’ll forgive them if I don’t have to pay any tax on the sale of Plantic,” Merchant wrote. “I would have thought with the amount of money put in to Plantic being equal to the sale and without ever showing a profit I shouldn’t have to pay tax?”

The Federal Court ruled Gordon Merchant used advice given by EY. Natalie Boog

By August 2014, Burgess had come up with a plan to deal with Merchant’s loans to Plantic, held in three separate companies.

“We are thinking that it is going to be best to make it a requirement under the SPA [share purchase agreement] that all loans from associated entities are waived or forgiven. That is, essentially the vendor pays the full ‘business value’ to [Merchant Family Trust and related entities and they] agree to write off any amounts owing by Plantic,” the EY partner wrote to McGrath.

Making the loan forgiveness a condition of the deal would boost the sale price (because a buyer would normally factor debt into a price), meaning a larger amount would be paid into the family trust.

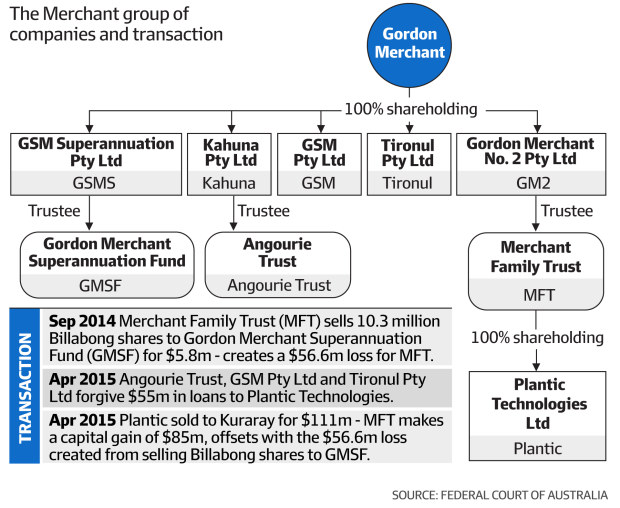

Ahead of the sale of Plantic, Merchant’s family trust sold more than 10 million Billabong shares to another of his companies for a little more than $5.8 million, resulting in a capital loss of $56.6 million, in September 2014. This was considered by the Federal Court to be a wash sale.

Burgess even acknowledged to one of Merchant’s employees there were risks, including “wash sale issues”.

“There are perhaps some slightly increased risks around a share sale given the debt forgiveness issues (e.g. commercial debt forgiveness rules, deemed dividend rules, direct and indirect value shifting rules) and sale of [Billabong] shares which crystallise capital losses (‘wash’ sale issues),” Burgess wrote on August 21, 2014.

“However, on balance we think these are manageable particularly given a forgiveness of related party debt is a common aspect of a share sale transaction and there are real commercial consequences of the super fund acquiring the shares (i.e. it is fully exposed to future share price movements/dividend policy).”

Wash selling is a sale of assets usually done to create a loss to use for tax deductions.

The three entities that extended the loan to Plantic would avoid having to pay a top-up tax related to income from a loan repayment because the loans were forgiven and the larger amount of money went to the trust for shares in the bioplastics firm. This is known as dividend stripping.

Tax implications

As negotiations with buyers continued, Burgess reinforced to Plantic chief executive Brendan Morris the tax implications if a deal was reached without forgiving the $55 million in loans.

“If the purchaser did not agree to a debt forgiveness as part of a share sale (i.e. instead paid less for the shares and injected further capital into Plantic to enable it to repay the loans), the tax costs associated with a share sale would be much higher,” he wrote in November 2014.

By March 2015, Japanese firm Kuraray had come in to buy Plantic.

Merchant’s trust would use the loss stemming from the Billabong share sale to reduce tax on the $111 million sale of Plantic in April 2015, offsetting $85 million in capital gains.

In 2020, the ATO issued new tax assessments to Merchant for the 2015 financial year following an audit of nine companies and trusts. The new notices increased Merchant’s personal tax bill by $30.6 million. Two of his firms were assessed to owe a further $12.9 million and were issued a $6.4 million penalty.

An EY spokesman said the consulting firm was not a party to the Federal Court case. Neither EY nor Burgess gave evidence.

“The findings of the Federal Court proceedings go to Mr Merchant’s commercial decisions and how these decisions impacted the tax outcomes,” the spokesman said.

“The judgment only reflects portions of the advice provided by EY, and may be the subject of an appeal. It is too early to characterise the judge’s findings as conclusive determinations regarding EY’s advice.”

EY and Burgess have filed defence in the proceeding brought by Merchant in the Supreme Court of Queensland.

“The findings in the Federal Court are not determinative of the matters in the Supreme Court case against EY, and no conclusions should be drawn in relation to EY based on those findings,” the EY spokesman said.

Merchant’s lawyers declined to comment.

Tax leaks scandal

Greens senator Barbara Pocock, who is a member of parliamentary committees scrutinising the accounting and consulting industry following the PwC tax leaks scandal, said the judgment raised questions about whether tax promoter penalties were strong and broad enough to deter these kinds of structures.

“EY have really landed their client in hot water here with tax advice that has clearly overstepped the mark,” she said.

“This is yet another example of the absence of any form of moral compass when it comes to making a buck for the big four. We understand that helping people to minimise their tax is what these firms do but the complete lack of any ethical boundaries, which in this case has led the client to a very costly outcome, is a stain on their profession.”

Emeritus professor of accounting at University of Technology Peter Wells said the judgment showed the whole structure created for Plantic’s sale was contrived to get out of paying tax.

“It reinforces the view that some people’s attitude to tax is different from the rest of us, it does raise questions about the artificial way transactions are being structured purely with the intent of avoiding tax,” Wells said.

Wells said there was a culture of developing structures in the tax sector, and the big four attempted to use legal professional privilege (LLP) to try to conceal them from the Tax Office.

Last July, The Australian Financial Review revealed PwC Australia settled false claims over 150 documents related to its tax advice for a multinational client.

“You’d have to hope the Tax Office is pursuing these strategies and that it’s a priority to give the Tax Office better tools to identity when these arrangements are being entered into,” he said.