Conventional wisdom is that sharemarket indices in advanced economies will provide a total return to investors including dividends of around 10 per cent per annum over the long term.

The S&P/ASX 200 total return index grew at a compound 8.1 per cent over the decade to June 7, 2024, while the Nasdaq 100 index of North America’s leading technology companies posted a compound annual growth rate of 16.6 per cent between July 2007 and April 2024, according to data provider Curvo.

Start young

Horton says the most important thing an investor can do to take advantage of compound interest is to start as young as possible.

“The earlier you start investing, the more time your money has to grow. Even modest investments can become large over decades,” she says. “Being consistent and investing over the long term is important because regular contributions – no matter how small – add up over time.”

Somebody who invested $10,000 in the Nasdaq 100 index in 2007 and added just $500 a month would be sitting on $724,707 today (before fees such as brokerage costs), based on its compound return of 16.6 per cent.

A more modest total return of 10 per cent per year would turn a $10,000 initial deposit into $452,965 in savings with just $500 added each month, over 20 years (see graphic above).

Or, if you inherited a lump sum of $500,000 at age 35 and earned 12 per cent for 15 years with $1000 added monthly, you would have savings of $3.5 million by the time you reached 50.

Understand risk and reward

Investment returns are inversely correlated to risk. This means you can earn between 4 per cent and 5 per cent at a big four bank today, risk-free.

However, if you seek higher returns, you must take on more risk of capital losses – ie, the value of your investments swings more in a process called standard deviation, as a measure of volatility over time.

Horton says time and a willingness to regularly save come rain or shine are all you really need to get rich and ride out volatility.

For example, she says a 25-year-old could reach a net worth of $1 million by 60 if they invested $600 a month, assuming an average annual return of 8 per cent. But if they waited five more years to start investing, they would have to invest $900 a month just to reach that same $1 million goal.

Samantha Horton says small savings can turn into huge sums if an investor stays disciplined and follows some simple rules.

Watch fees

If you invest regularly over a long period of time in shares or exchange-traded funds (ETFs) that track the performance of indices, brokerage and management fees can add up – although the emergence of discount brokers means it’s cheaper than ever to buy shares direct.

Standard ETFs that track sharemarket indices such as the S&P/ASX 200 or Nasdaq tend to charge annual management fees from 0.1 per cent to 0.5 per cent. “When fees are deducted, the remaining investment has less capital to grow,” Horton says.

“The compounding effect of this means that higher fees can substantially reduce your investment’s potential growth over the long term. Some funds also have additional costs, such as entry and exit fees or performance fees, that can further diminish your returns.”

The difference between 0.3 per cent and 1 per cent per year may not sound like much. However, $100,000 invested for 20 years on an average annual return of 8 per cent and a 1 per cent management fee, would grow to about $386,970. The same investment with a 0.3 per cent management fee would grow to around $440,870.

“That’s an additional return of $53,900,” Horton says. “Put another way, that’s 53.9 per more on your investment over time.”

If you assume you pay at least $5 a trade at a typical discount broker, that would equal $60 a year in brokerage costs based on one trade a month, or $600 over 10 years.

Problem with timing the market

Once you adjust for fees, the correct behaviour to manage your investments is important to master. One of Wall Street’s most famous investors Peter Lynch said that “more money is lost by investors trying to predict market crashes than in the actual crashes themselves”.

Lynch means the key to getting rich from shares is not getting spooked into selling by scary headlines or gloomy predictions of imminent crashes.

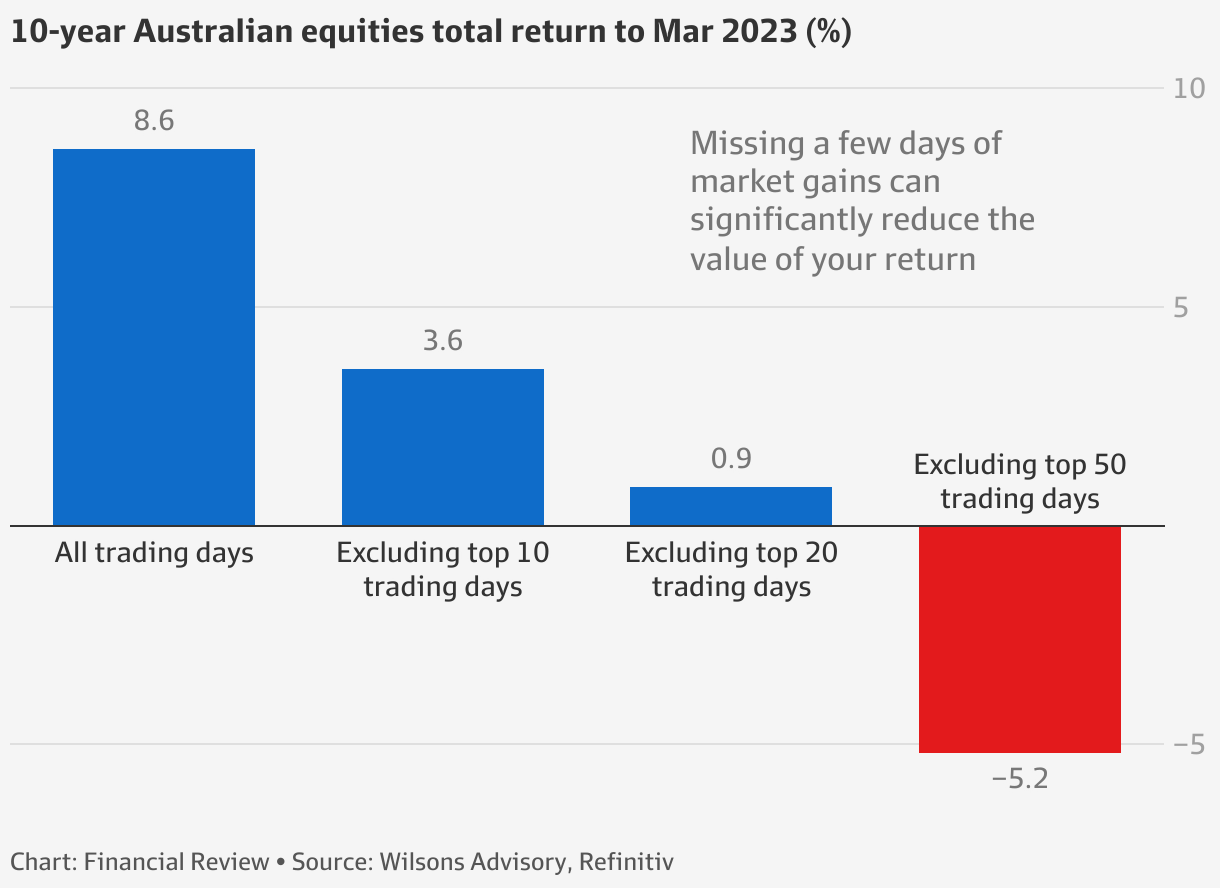

Now 80, Lynch returned 29.2 per cent per year running Fidelity’s Magellan Fund between 1977 and 1990 and said not missing out on the market’s strong days was another key to high returns.

The chart below from Australian financial advice group Wilsons Advisory shows how missing out on the market’s strongest days because you sold out and tried to time the market can hammer your returns.

Australian fund manager Emanuel Datt, founder of Datt Capital, agrees that retail investors are better off ignoring the regular calls around imminent market crashes.

“Ultimately, if you’re a retail or passive investor you’re not looking at markets every day, so staying power is an underappreciated quality,” he says.

“I remember back in February everyone said the market [S&P/ASX 200] would crash – instead it has mooned from under 7000 points to 7800 so it’s run 10 per cent despite dire predictions. That’s why I encourage staying for the long term.”

Datt, whose Datt Capital Absolute Return Fund has returned 19.7 per cent annualised since inception in 2018, adds that more sophisticated investors may try to time the market to take advantage of a phenomenon known as tax loss selling.

This is where investors sell shares to deliberately book a loss in the months before the financial year-end of June 30. This is so they can offset losses against capital gains tax on profitable investments.

“There’s definitely a seasonality in Australian markets,” Datt says. “May and June are softer months for shares and a lot of that comes down to people trying to reduce tax bills. July has a very high statistical probability of being positive.”

Remember the taxman

Anyone lucky enough to generate capital gains in the sharemarket over 10 years or more will face some important considerations. First, remember the Australian Tax Office will take its share of gains if you sell shares to realise cash profits.

Capital gains tax (CGT) is part of an income tax return and means any profits on investments sold are added to your total income at the end of the tax year and taxed at your income tax rate.

“People often misunderstand that CGT is not a separate tax – the net capital gain goes on top of your income and is taxed at marginal rates,” says Ben Turner, managing director of tax accountant Atlas Wealth Management.

If an investor holds shares for more than one year, they’re entitled to 50 per cent of the capital gain tax-free. This means an investor pays CGT on $500 of a profit of $1000 on a $10,000 investment held for more than a year. If the investment is held for less than a year, the investor must pay tax on the full $1000 gain.

Turner adds that other factors to consider include the cost base of shares under any dividend reinvestment plans and the ability to offset losses against capital gains.

“When selling shares, you need to ensure your purchase history is tracked adequately to determine the correct tax treatment on the sale,” he says. “Complications arise when you acquire shares over several purchases or subscribe to a dividend reinvestment plan.

“For example, if you were to partially sell your shares in a particular company, you need to nominate and track which shares you are selling and their cost, which will differ between purchases.”

Assuming a sharemarket investor makes profits of $450,000 over 20 years on an initial $10,000 investment, they would have to pay CGT on $225,000 in profits at their marginal income tax rate, as half or 50 per cent of the $450,000 profit is tax-free.

From July 1, income will be taxed at 45 per cent above $190,000, so $35,000 of the $225,000 in profits would be taxed at 45 per cent. The remainder of the $190,000 in profits would be taxed at marginal rates.