{kind=link}

New Zealand mortgage commitments continue to rebound slowly after bottoming out in late 2022.

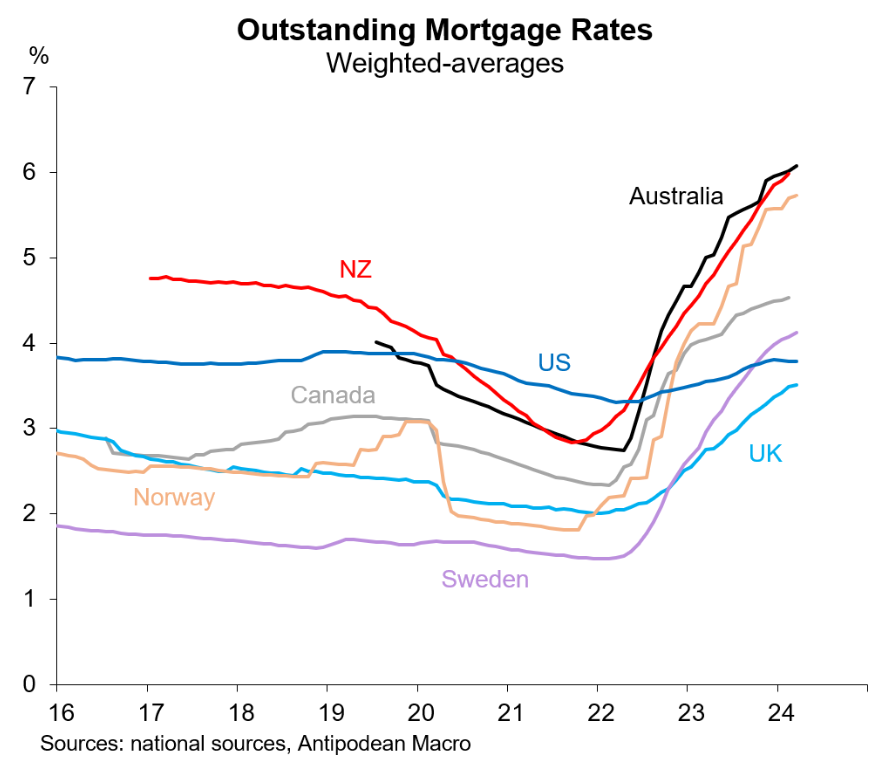

The modest rebound in mortgage commitments follows the sharp increase in mortgage rates following 5.25% of official interest rate hikes by the Reserve Bank:

Advertisement

With New Zealand’s economy suffering a technical recession and deep per capita recession, the Reserve Bank is poised to commence a rate easing cycle either late this year or early next.

When the Reserve Bank starts cutting rates, it risks fuelling another house price boom.

Accordingly, the Reserve Bank has confirmed the activation of new debt-to-income (DTI) restrictions and the slight loosening of loan to value ratio (LVR) limits.

Advertisement

The new DTI restrictions will limit the amount of high-DTI lending that banks can make, while LVR restrictions limit the amount of low-deposit lending they can make.

Below are the new DTI limits banks will have to meet:

- 20% of new owner-occupier lending to borrowers with a DTI ratio over 6; and

- 20% of new investor lending to borrowers with a DTI ratio over 7.

Advertisement

The current LVR settings are:

- 15% limit for loans with LVR above 80% for owner occupiers, and

- 5% limit for loans with LVR above 65% for investors.

LVRs will be eased to allow banks to make:

- 20% of owner-occupier lending to borrowers with an LVR greater than 80%; and

- 5% of investor lending to borrowers with an LVR greater than 70%.

Banks will need to comply with the new DTI and LVR restrictions from July 1, 2024, and will apply to new lending for residential properties in New Zealand, for both owner-occupiers and investors.

Advertisement

David Hargreaves at Interest.co.nz explained that the current number of new mortgages being approved on high DTIs is well below the proposed limits.

However, that “could and likely would change in the next housing market upturn – and it’s not so long ago that the numbers of new mortgages on high DTIs was rocketing. So, that’s when the DTI limits would really come into play”.

Placing limits on high DTI lending is sensible and is likely to dampen the next upswing in home prices, as well as improve financial stability.

Advertisement

Preventing a problem from occurring is always better than trying to close the regulatory gate after the mortgage horse has already bolted.